Simply mention the word “taxes” and the reaction that you will get from most business owners and individuals is one of disgust, frustration, or irritation. The fact is that taxes will always be part of your financial life, even despite recent election results, and creativity can be the key to managing your tax liability.

Take for instance our client, James, who owns a successful closely-held corporation. James, like many of our retirement plan sponsors, was interested in ways to use company-sponsored retirement plans to reduce his tax burden. He already had a 401k plan in place but wanted to do more. Since he and his key executives were considered “Highly Compensated Employees” by IRS standards, they were limited in their ability to defer income from their lucrative positions.

Take for instance our client, James, who owns a successful closely-held corporation. James, like many of our retirement plan sponsors, was interested in ways to use company-sponsored retirement plans to reduce his tax burden. He already had a 401k plan in place but wanted to do more. Since he and his key executives were considered “Highly Compensated Employees” by IRS standards, they were limited in their ability to defer income from their lucrative positions.

Alternatives to 401k

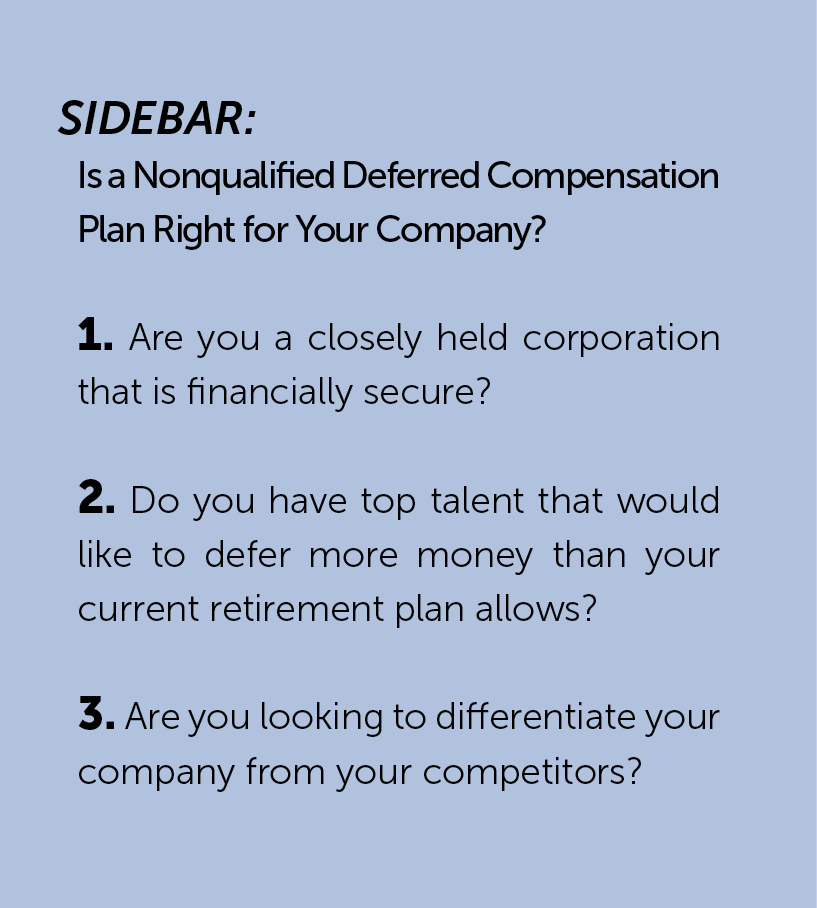

We recommended a supplement or alternative to their 401k called a Nonqualified Deferred Compensation (NQDC) plan. This type of plan offers a creative design option that may help your company’s highly compensated employees put away additional retirement dollars. This type of plan can be an effective retirement planning tool, especially for owners of closely-held corporations. They give owners and employees the ability to accumulate significant wealth because they allow assets to compound tax-free over time and frequently offer attractive investment options.

Take an executive, like James, who makes $300,000 per year and who currently defers the maximum allowed into his company’s 401(k) plan; $18,000 for 2017, plus an additional $6,000 since James is over 50 years of age. The $24,000 deferral amount only represents 8 percent of his annual income rate, which is more than likely not enough to get him to the typical goal of between 70 to 90 percent of income that needs to be replaced for retirement purposes. Plus, it leaves him with a significant amount of taxable income.

A Nonqualified Deferred Compensation plan may allow James to put away much more for retirement helping him get closer to his retirement goals and it can help reduce his tax liability in the current year. Let’s take a closer look at these plans and their design features. The description below is only meant to be an introduction. Careful consideration of your company’s tax situation, long-term goals, and funding obligations must be given before any specific recommendations can be made.

A Nonqualified Deferred Compensation plan may allow James to put away much more for retirement helping him get closer to his retirement goals and it can help reduce his tax liability in the current year. Let’s take a closer look at these plans and their design features. The description below is only meant to be an introduction. Careful consideration of your company’s tax situation, long-term goals, and funding obligations must be given before any specific recommendations can be made.

Compensation in the Future

The NQDC plan is a contract between the employer and the employee or independent contractor to provide compensation to the employee at some time in the future in lieu of compensation paid today. The plans are nonqualified for two reasons; first, the plan does not fall under the protection of the Employee Retirement Securities Act (ERISA) and second, the same tax benefits are not applied to NQDC plans as they are to qualified retirement plans, such as your 401(k). It is important to understand these two distinctions.

Since the assets are not protected under ERISA, they remain assets of the company and therefore are subject to the liens of general creditors. In addition, the employer typically deducts the expenses when the income is recognized by the employee unlike in a qualified plan when tax deductions are credited to the employer at the time the benefits are set aside.

The difference in taxation is known as the doctrine of constructive receipt. This concept states the nonqualified plan benefits are taxable to the employee at the time the employee has the right to receive benefits, regardless of when the benefits are actually paid, unless the employer’s promise to pay remains unfunded or unsecured.

Note that it is typically preferred that the promise to pay remain unfunded to meet the goal of tax deferral. While constructive receipt sounds confusing and a little intimidating, it is one of the most powerful aspects of the NQDC plan when it comes to retaining top talent since it encourages the participants in the plan to stay with the company until retirement to avoid receiving benefits prior to retirement age. This is why NQDC plans are also sometimes referred to as “golden handcuffs.”

Note that it is typically preferred that the promise to pay remain unfunded to meet the goal of tax deferral. While constructive receipt sounds confusing and a little intimidating, it is one of the most powerful aspects of the NQDC plan when it comes to retaining top talent since it encourages the participants in the plan to stay with the company until retirement to avoid receiving benefits prior to retirement age. This is why NQDC plans are also sometimes referred to as “golden handcuffs.”

The plan’s lack of qualification also allows the employer to discriminate freely amongst employees. To clarify, the nondiscrimination rules that apply to qualified plans, like your company’s 401(k) plan, do not apply to NQDC plans. Thus, an employer can choose to benefit a select group of employees, regardless of their classification as highly compensated or non-highly compensated (note a highly compensated employee for 2017 is an employee that earns over $120,000).

There is also no limit to contribution amounts to the plan unlike the 415 limits that apply to qualified plans. Remember in James’ example, he could only defer $18,000 plus a catch-up amount of $6,000 into the 401(k) plan. With NQDC plans, the amount that can be deferred into the plan can be either determined by the company or by the individual participant.

About the Authors

Trent, Valerie and Jamie are best known for taking complex financial problems and offering customized solutions to their client’s problems. Their firm, Grinkmeyer Leonard Financial, is widely recognized as one of the top investment advisory firms in the U.S. and their services range from retirement plan consulting for companies to investment management and individual financial planning for individuals.

Disclosures: Trent Grinkmeyer, Valerie Leonard, and Jamie Kertis are Registered Representatives and Investment Adviser Representatives with/and offer securities and advisory services through Commonwealth Financial Network, Member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services offered through Grinkmeyer Leonard Financial, Grinkmeyer Leonard Benefits Group, or CES Insurance Agency. Grinkmeyer Leonard Benefits Group and their leadership consulting services are separate and unrelated to Commonwealth. This communication is not intended to replace the advice of a qualified tax advisor or attorney.

{kind=link}